As 2025 ends, the global economy shows remarkable resilience despite trade tensions, policy uncertainty, and lingering inflation pressures. Global growth held steady around 3.2 percent this year, supported by AI-driven investments, improved financial conditions, and strong trade volumes. However, forecasts point to a slowdown, with the OECD projecting 2.9 percent growth in 2026 before a slight recovery to 3.1 percent in 2027. Central banks navigate diverging paths, while record trade surpluses and widening inequality highlight structural imbalances.

A standout development is China’s goods trade surplus surpassing $1 trillion for the first 11 months of 2025, reaching $1.076 trillion. This record comes from booming exports to emerging markets like Africa and ASEAN, offsetting sharp declines to the US due to tariffs. China pivoted effectively, with strong growth in electronics and electric vehicles. Yet this surplus underscores reliance on exports and calls for greater domestic consumption.

Global trade remains a bright spot, on track to exceed $35 trillion in 2025 according to UNCTAD. Growth shifted to volumes rather than prices, led by East Asia, South-South trade, and AI-related sectors. Trade outpaced GDP, reversing prior stagnation, though momentum may weaken in 2026 amid higher costs and uncertainty.

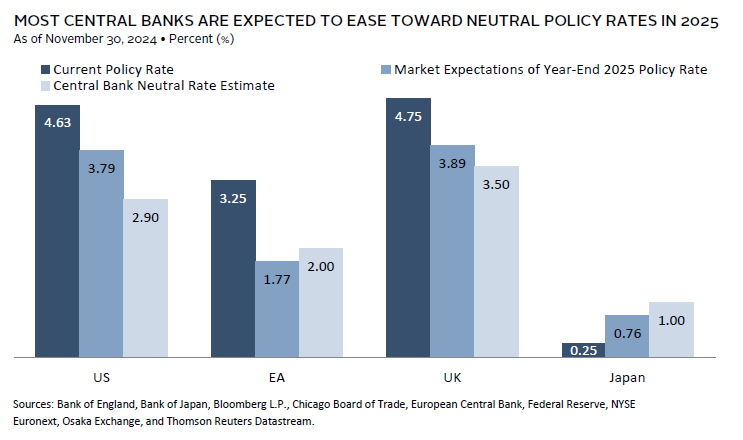

Central banks face tough choices. The US Federal Reserve cut rates by 25 basis points in December to 3.5-3.75 percent, prioritizing labor market cooling over elevated inflation. Services inflation accelerated in Europe, prompting caution ahead of the ECB’s December 18 meeting. Diverging policies reflect regional pressures from tariffs and fiscal concerns.

Inequality persists as a challenge. The richest 10 percent own 75 percent of global wealth, with the top 0.001 percent holding more than the poorest half of humanity. Reports emphasize how concentrated capital drives disparities, calling for policy action.

Global Economic Outlook (January 2025): Divergent Growth and …

Looking ahead, cooperative trade resolutions and vigilant monetary policy will be key to sustaining resilience. While 2025 defied downturn predictions, underlying risks from protectionism and inequality demand attention for balanced growth in 2026 and beyond.